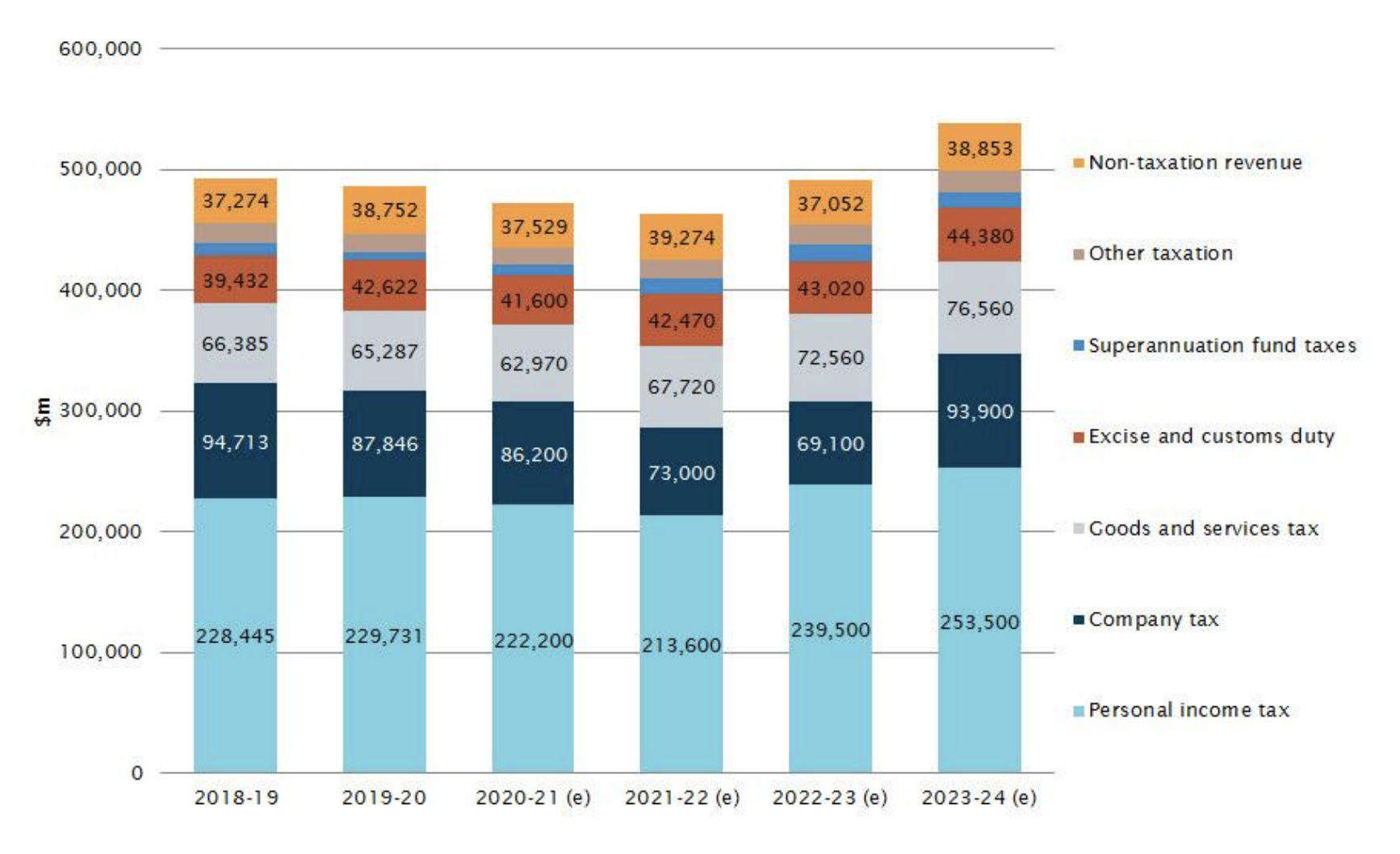

The Figure illustrates Australian Government revenue by its major components. Personal income tax (income tax withholding) is, by a margin, the largest component of Australian Government revenue, accounting for around 47.2 per cent of total Government revenue in 2019–20.

Company tax is the second largest component, accounting for around 18.1 per cent of total revenue, followed by goods and services tax (13.4 per cent), excise and customs duty (8.8 per cent) and non-tax revenue (8.0 per cent).

Indirect Taxes

Indirect taxes are taxes which are generally applied to goods and services as opposed to income or profits.

They are called indirect taxes because the ultimate burden of the tax generally does not fall on the entity that pays the tax

It is levied on suppliers of goods and services, but the incidence of the tax generally falls on the end consumer through higher prices.

Australia’s largest indirect taxes are the GST, excise and customs equivalent excise duties on the manufacture and importation of fuel, alcohol (excluding wine) and tobacco products, and import tariffs.

Smaller indirect taxes include the luxury car tax and wine equalisation tax.

Composition of Government Expenditure

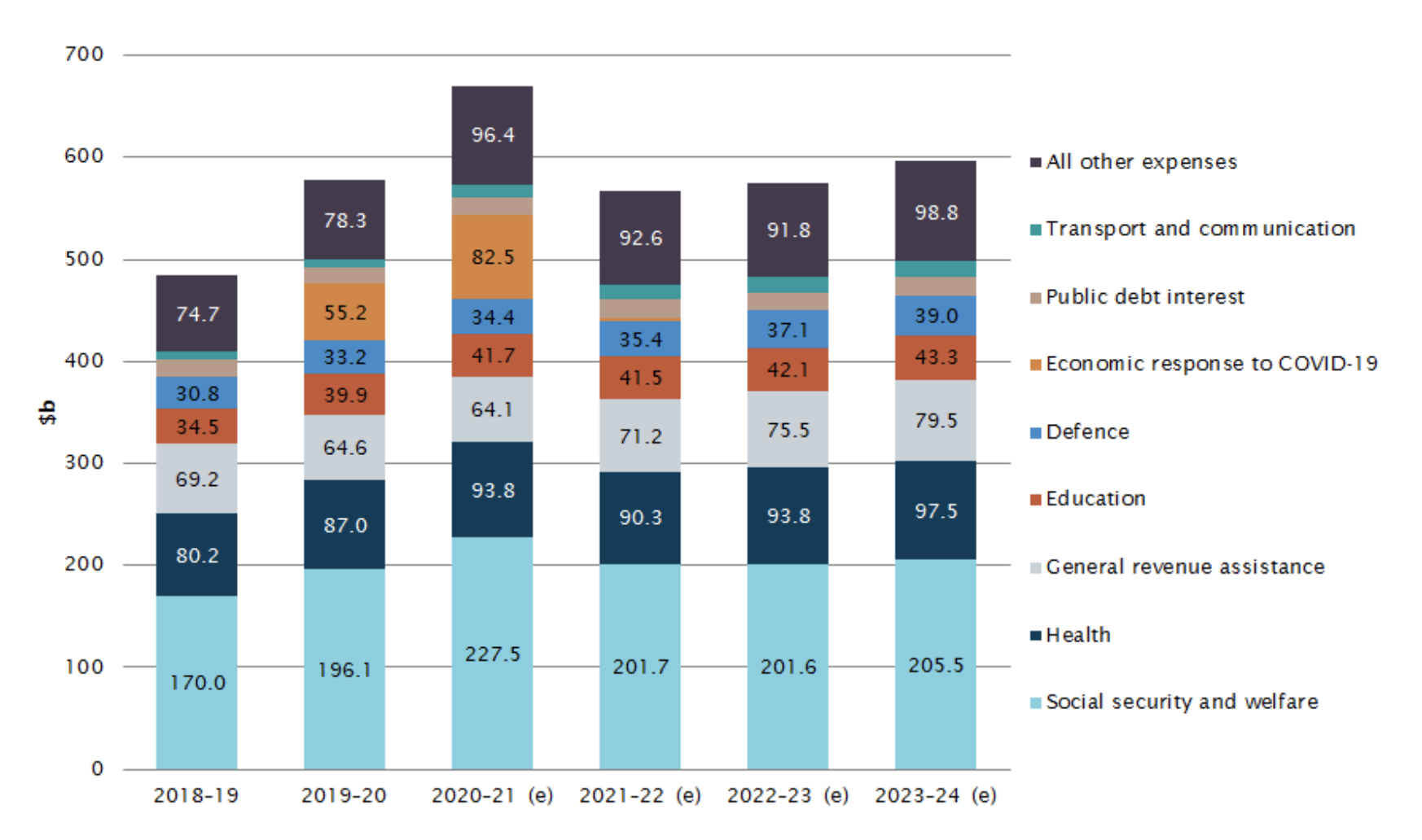

Social security and welfare is the largest functional expenditure of the Australian Government accounting for just over a third of all Government expenditure.

This function includes age pension expenditure, family tax benefits, child care subsidies, JobSeeker payments and the National Disability Insurance Scheme.

The social security and welfare expenditure budget brief provides more detail on this expenditure.

Health expenditure, which includes Medicare expenditure and Australian government expenditure on hospitals and aged care, accounted for around 15.0 per cent of all Australian Government expenditure in 2019–20.

The COVID-19 pandemic has led to an increase in expenditure on health, as discussed in the public health response to COVID-19 budget brief.

General revenue assistance is money paid by the Australian Government to the States and Territories and local government to spend on any purpose (also called ‘untied’ funding).

This is distinct from funding provided by the Australian government to other levels of government for agreed specific purposes such as building hospitals, infrastructure or funding schools.

This expenditure is largely payments of the goods and services tax, which is collected by the Commonwealth but transferred to the states and territories.

General revenue assistance accounted for around 11.1 per cent of Government expenditure in 2019–20.

Education which includes Australian Government funding for primary and secondary education and tertiary education accounted for around 6.9 per cent of Government expenditure in 2019–20.

The economic response to COVID-19 includes the JobKeeper program and JobMaker Hiring credit and is expected to account for 9.5 per cent of Government expenditure in 2019– 20, growing to 12.3 per cent of expenditure in 2020–21.