Besides raising revenue, the taxation system plays an important role

In the redistribution of income from the wealthy to the poor.

Influencing how resources are allocated among users

In regulating the economic fluctuations with the business cycle.

Taxes can be classified according to their impact and incidence (burden).

Impact - ‘where the tax is levied or collected’

Incidence – ‘where the burden of the tax falls or who pays the tax

Concepts

Classification of taxes – from whom they are collected

Direct taxation is collected from the taxpayers’ (individual or corporate) income, so the impact and the incidence or direct tax fall on the same person

Indirect taxation (Excise tax, GST) are collected from consumer spending on a wide range of products. The impact and incidence of indirect taxes fall on different people. Eg. an excise tax, the seller of the good pays the tax, but then passes it on to the consumer through higher prices.

The seller collects the tax, but it is actually collected by the consumer.

The seller collects the tax, but it is actually paid for by the consumer.

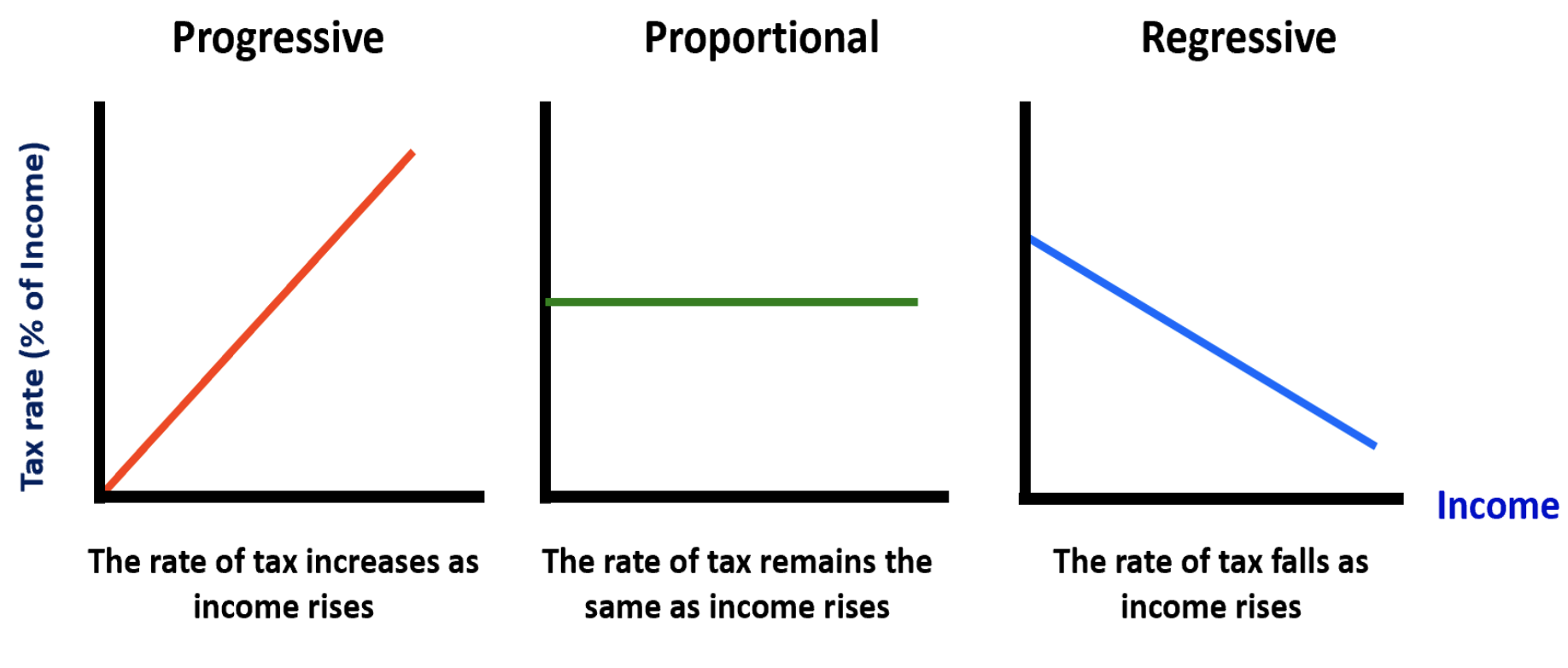

3 types of Taxes

Progressive Tax: The rate of tax increases as income rises

Proportional Tax: The rate of tax remains the same as income rises/falls

Regressive Tax: The rate of tax falls as income rises

Classification of taxes – How they are levied

Progressive Tax

Progressive taxes - claim an increasing proportion of income as income increases.

The Burden of a progressive tax falls mainly on those who earn higher levels of income.

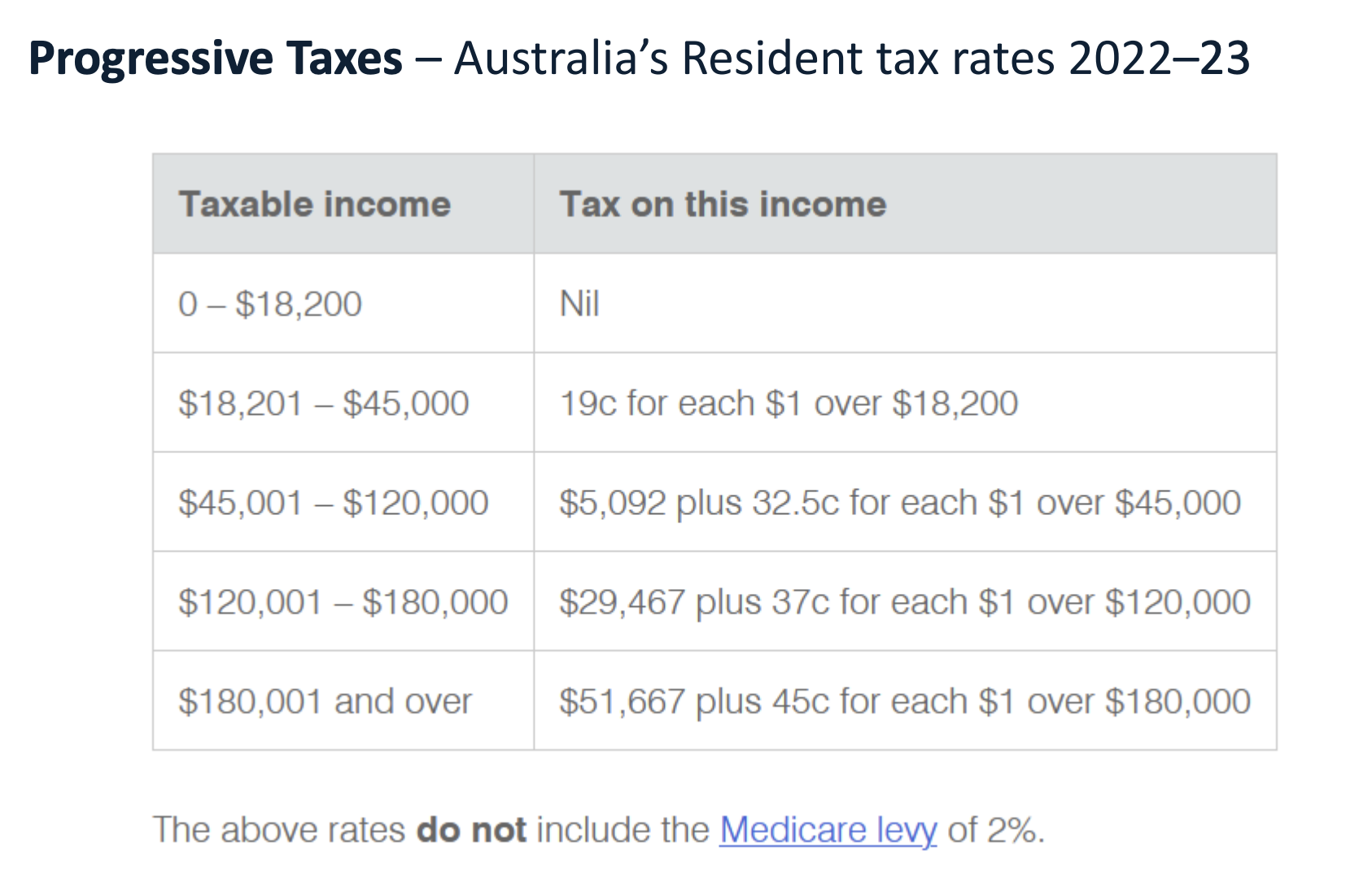

Australia, like many other countries, has a system of income tax ‘brackets’ which create a ‘stepped relationship between income and tax payable.

Regressive Tax

Regressive Taxes – place a greater burden on lower income earners because they take a decreasing proportion of income as income increase.

eg. An excise tax levied at a flat rate on an item such as a box of chocolates.

The low income earner will pay the same dollar value of tax on the chocolates as does the high income earner.

To the low income earner, however, the tax is a higher proportion of their income.

Proportional Taxation

Proportional Taxation – takes a constant proportion of income, no matter what level has been earned.

The best Australian example of proportional tax is company tax, where all companies, irrespective of size earnings, currently pay tax at the rate of 30 percent of their profits.

Specific Tax

Charged on the volume of sales regardless of price

Ad Valorem (Value Added Tax)

Levied as a percentage of price

Types of Taxes

Classified based on sources of tax revenue.

Tax bases:

Income

Good and services

Property and Wealth

Classification of taxes – Source of Tax revenue

Taxes on income – levied on all wage and salaried income, at rates which specify how much of the last (marginal) dollar will be paid as tax.

Personal income tax - is direct, as the impact and incidence of the tax both fall on the same person.

Income tax has a progressive burden, as marginal tax rates rise as income rises.

People on higher incomes pay more tax, both in money terms, and as a proportion of their income.

Company tax (corporate tax)– a proportional tax whose impact falls on the individual company, even, though the incidence probably falls on consumers because the tax is a cost of production that is passed on to buyers.

Since 2001 the rate of company tax has been 30 cents to the dollar (companies with turnover less than $10million pay 27.5 cents)

Taxes on the Provision of Goods of Services

Good and Services Tax (GST) – Broad based tax levied at 10% of the price of most goods and services consumed in Australia.

The impact of the GST falls on the seller of the good or service

The incidence (burden) falls on the consumer. GST revenue is collected by the federal government and distributed to state governments.

It is thus regarded as a state tax

Excise duties – imposed at a flat rate on domestically produced goods such as alcohol; cigarettes; oil products ; and LPG (gas).

Excise raises a great deal of revenue for the government often without affecting consumption patterns because they are levied on price inelastic goods

Intended to reduce social costs/externalities that these types of consumption may have on the community.

Customs duties – an indirect tax levied on many imported goods (ie a tariff) , often as a means of protecting Australian producers from overseas competition.

Taxes on Property and Wealth

Capital Gains Tax (CGT) - a progressive tax which is levied on capital gains (profits) from the sale of assets held for a period longer than 12 months (any asset sold within 12 months is subject to tax at the income earners’ normal marginal rate).

The CGT burden is adjusted for inflation, so any profit on the sale of the asset is adjusted according to the change in the CPI since the asset was purchased.

The CGT does not apply to assets purchased before Sep 19 1985 nor to personal items eg. cars houses boats

CGT applies to shares investment properties business goodwill and some personal items if they were purchased with the intention of resale (eg jewellery)

Income Redistribution - Direct Taxation

Income Redistribution through Direct Taxation: Personal Income Tax – is progressive so high income earners pay a greater proportion of their income in tax than low income earners.

Government Spending - utilised to redistribute income.

Direct transfer payments - (pensions and welfare benefits) provide direct income support for the aged; the unemployed; the sick and disabled; sole parents and children (family allowance)

Social security and welfare accounts for the greatest proportion of Commonwealth Government Spending in Australia – about 40 percent pf budget

Indirect government payments also redistribute income:

Public services like

Education

Housing

Healthcare

provided at less than their full cost - subsidised by government

These subsidies help redistribute income and enable all Australians to have access to basic services

If these services were to be provided by the market, it is likely that some households would not be able to afford them, end they would end up not consuming them (underconsumption)